What is the Rate of Return Myth?

Did you know that two accounts can average the same return over a fixed period of time and actually end in very different results. Confused? That's OK, let us explain. But first, in one of our other articles, we explain a concept called Sequence of Returns Risk. The Rate of Return Myth builds on this information to further illustrate why average return may not tell the whole story-- so we're going to dive a little deeper.

For our example, take the following into consideration:

- We have two accounts, each starting with $1 million.

- One account is tracking the S&P 500 and is taking on the full ups and downs of the market during an 22-year period.

- Another account focuses on less volatility across the same timeline.

- Both accounts average the same return over the 22 year period.

[Disclosure: Hypothetical performance results have been provided for general comparison purposes only. Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable or equal the corresponding indicated performance level(s). Hypothetical returns using S&P 500 annual returns for respective years listed above.]

Surprisingly, despite both accounts showing an average return of almost 9.49%, the low volatility account ends up with nearly 20% more at the end of the period. The chart above helps illustrate the Rate of Return Myth--The idea that average return in a given year is the primary factor influencing account growth. In reality, it is the amount of principal in the account in the beginning of each year that truly drives long-term success.

Simply put; It is not about the return received in a given year, it is about the amount of money you are getting the return from.

How does a Low Volatility Account work?

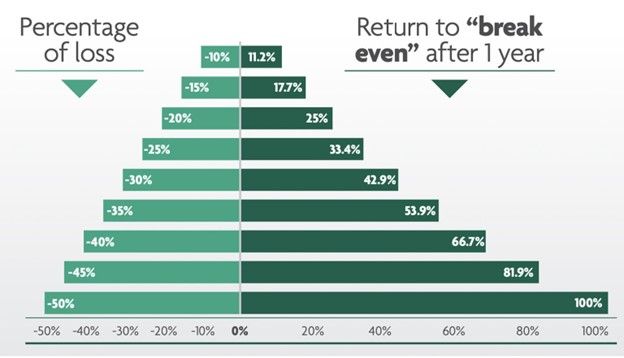

By adopting the low volatility approach in parts of your portfolio, you may miss out on exceptional years that generate high returns of 25-30% or more. The trade-off is that you also avoid the devastating lows of -23% and -38%. Many people tend to misunderstand is the "Break-even Burden" that follows some of these market corrections and downturns:

Source: Copyright North American, all rights reserved.

Downside protected strategies uses many techniques outside of traditional bond investments to limit losses and help safeguard your hard-earned savings from significant losses. This low volatility approach aims for a much smoother and consistent growth trajectory for accounts you wish to protect.

High Risk Investing:

- Takes on extreme highs and extreme lows of the market.

- Tied to more uncertainty.

Low Volatility Approach:

- Focuses on stability

- Provides peace of mind

- Allows you to weather market downturns without losing sleep

Do I need to be taking on a lot of risk?

Consistency and discipline play pivotal roles in achieving your most important financial goals. If you're only a few years to retirement, prioritizing preservation of capital and minimizing downside risk, you can build a solid foundation for future growth.

It may be time to reevaluate your investment options, don't be lured by the Rate of Return Myth. Consider the bigger picture and choose a strategy that aligns with your current goals and timeline.

This article is provided by McAdam LLC (“McAdam” or the “Firm”) for informational purposes only. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this article is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax, or legal advice. Certain information contained in this report is derived from sources that McAdam believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. This article is the sole opinion of this individual and is not indicative of the firm’s belief.

Related articles