Retirement Planning Checklist

Retirement planning can elicit a wide range of emotions. Everyone looks forward to financial freedom, post-work traveling, sleeping late during the week, and finally leaving the workforce. There's also the concern of running out of money, boredom, or making a major financial mistake that might result in a massive tax burden.

The most effective strategy to deal with your anxieties is to plan ahead. The sooner you start planning, the better. You're already ahead of the game if you're thinking about retirement now, and to assist you more, use this checklist as the foundation for your planning.

1. How much should I have saved for Retirement?

There are a lot of important numbers you'll discover throughout the course of retirement. They're valuable in the grand scheme of things—and sometimes only for their ability to instill fear. For example, they can tell you if you're falling behind on your savings.

You should always be aware of concepts such as the 4% rule and the 80% rule— the latter suggests that your expenses will drop by about a fifth after the working years as compared to your last year in the workforce. Then there's the 25x rule: in order to figure out how much you need saved up to retire comfortably, simply multiply your annual expenses by 25. For example, you'll need to have $2 million saved if your yearly expenses tally $80,000.

Understanding these numbers can offer a quick, high-level view of how your retirement may play out, creating a basis of what the real numbers may be.

2. Calculate your Net Worth

Get an understanding of your current net worth: list out all of your assets and liabilities-- cash, 401(k), IRAs, annuities, insurance policies, property, & mortgages, loans, etc.-- have a firm grasp on your personal balance sheet as well.

This advice may seem self-evident, but you may overlook something important, such as how your available income may alter depending on when you decide to turn on Social Security. Another example is how drastically your investment returns can shift in five years or how much "the final nest egg" you come up with might be absorbed by inflation and taxes.

3. Use a Financial Professional

When it comes to planning, any sort of financial management or a financial planner can be extremely beneficial. Although many folks are employing professionals ineffectively. There is a large number of advisors out there acting as a costly source of stock picking rather than focusing on estate planning and tax strategies, the crucial work of a CERTIFIED FINANCIAL PLANNER™ (CFP).

80% of households with a financial advisor relied on them primarily to make investment suggestions, according to a TransAmerica survey. 31% of people employed a professional to determine income needs, 23% put together 401(k) withdrawal strategies, and only 21% had any sort of focus on tax planning.

That 80% number represents the inverted perspective on how to make the best use of professional financial management. Many people can invest money on their own, but they require the most assistance when it comes to turning their nest egg into a consistent, long-term income strategy.

4. Strategize your Retirement Spending

A lot of new retirees misjudge the increased first-year costs of retirement. You'll undoubtedly spend more on vacation than you anticipated, using private healthcare prior to Medicare may result in higher costs, as well as closing fees if you downsize your house.

Calculating your future income from Social Security, annuities, and pensions is the first step. Then building a strategy around your spending capabilities can help take out the guessing-game of how long your nest egg will last you. It will also create a sense of security knowing you'll have enough.

5. How to Withdraw from your 401(k)

Maximizing your income while limiting Uncle Sam's take can often be difficult. Maxing 401(k) pre-tax contributions are just one of the factors that go into your future tax bill. After the working-years, most people face a number of tax issues:

- Required minimum distributions (RMDs) from your qualified accounts

- 401(k)

- Traditional IRA

- Annuities

- Capital gains on selling the house

- Medicare income limits.

Something to consider is conducting a tax-saving Roth conversion after you retire, prior to turning on Social Security. When your tax bracket is low, you should pay income tax on 401(k)s and Traditional IRAs and receive tax-free Roth withdrawals later in life.

That's just one reason why it's critical to plan 401(k) withdraw techniques. It can be difficult to juggle future taxes and making the wrong decision might cost you a lot of money. It's worthwhile to get a financial planner and professional assistance on your future tax bill.

6. Turning on Social Security

Most people are aware that those who delay turning on Social Security will receive higher monthly benefits— but are you aware of the difference? It can be very significant, as delaying until age 70 can increase benefits by approximately 75%.

Delaying is a good option if it works for your plan, but without planning ahead, you won't know the answer. When planning for Social Security, there are studies that explain how men often overlook the importance of their spouses' benefits. Women historically live longer than men, and many male retirees turn Social on earlier, negatively affecting their spouses' distributions later in life.

To summarize, plan ahead of time to utilize your qualified assets initially and defer Social Security benefits.

7. Plan for Medical Expenses, Including Long-Term Care

Medicare can be very helpful, but it may not cover everything. 1 in 5 Medicare enrollees pay for Medigap coverage, which costs around $150 per month. According to the Bureau of Labor Statistics, people aged 65 and overpaid more than $6,600 for healthcare in 2020. Fidelity ran a study and found that couples who retired in 2021 will require $300,000 to cover medical bills throughout the retired years.

If you plan to retire before Medicare benefits kick in, plan to shovel a lot more of your savings towards private health insurance.

Long-term care insurance, which covers nursing homes and assisted living, for example, is now a lot more popular. It can be extremely complicated, so don't wait until you or someone you care about can't live independently to start looking into it.

8. When should you Retire?

Continuing to work is a terrific approach to boost your nest egg and an easier route for financial freedom. Every dollar you earn is a dollar you won't have to take out of your nest egg.

Look into part-time work prior to handing in your resignation papers. AARP did a study back in 2019 and found that 20% of Americans over 65 are still working or looking for work. Any side business or part-time work can provide not only some income, but a little more purpose in retirement-- helping avoid any sort of boredom past the career years.

9. Understand that an Investment Account is NOT a Retirement Plan

Years ago, retirees would just put their money in CDs & T-bills and let their investments run themselves. That strategy, however, isn't as effective as it used to be. A recently retired 65-year-old must still focus on long-term investments with some sort of significant portion of their portfolio in equities.

There is always the short-term focus as well; the cash you'll need to cover living expenses over the next five years should be readily available in protected growth investments. Allocate at least 5 years’ worth of living costs in safer assets with higher liquidity. As you get closer to retirement, plan on gradually transitioning some of your long-term risky investments to more short-term, safe money strategies. Utilize the help of a CFP to get you on track for both short-term and long-term retirement savings.

10. How to Start Estate Planning

Ensure you leave the legacy you want after such a long, hard-working career. Does each of your accounts have a designated beneficiary? Is your will updated? Avoid future inheritance taxes for both you and your loved ones by gifting up to the taxable limitations.

Passing without any sort of estate plan will most likely place a huge financial burden on survivors and put them in a place where the IRS could step in and take a lot of your savings off the table. Avoid it through a proper, thorough, and comprehensive financial plan created by a CERTIFIED FINANCIAL PLANNER™.

Start Planning Today!

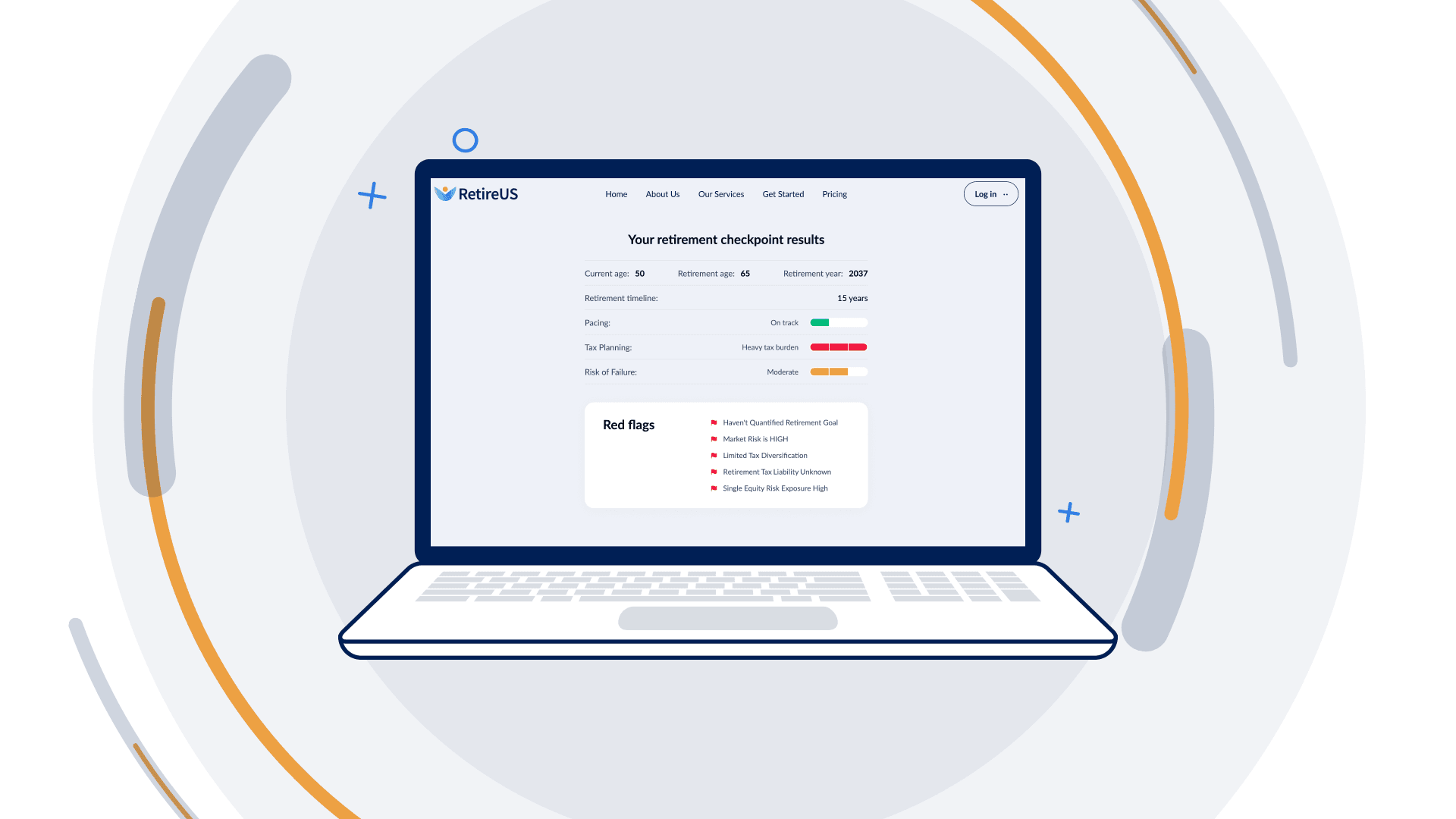

The path to financial freedom into retirement has many steps, but the quicker you start, the less headaches that are to follow once you get closer to the end of the working years. If you find yourself lost with any of these steps or don't know how to start, utilize our FREE Financial Checkpoint.

This article is provided by McAdam LLC (“McAdam” or the “Firm”) for informational purposes only. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this article is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax, or legal advice. Certain information contained in this report is derived from sources that McAdam believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. This article is the sole opinion of this individual and is not indicative of the firm’s belief. Any references made regarding the taxable nature of your investments should not be construed as tax advice. McAdam LLC is not a tax advisory firm; therefore, any tax decisions or assumptions should be made/verified with your tax professional.

Related articles