Know Your Options: Your Thrift Savings Plan (TSP)

By: Elias Park, CFP®, CRPC®

For federal employees, the Thrift Savings Plan (TSP) is one of the most powerful tools for building a secure retirement. Similar to a 401(k) for private-sector employees, the TSP allows federal workers to save and invest for their future through tax-advantaged contributions and diversified investment options.

As retirement approaches, understanding how your TSP works—and making informed decisions about contributions, investments, and withdrawals—can significantly impact your retirement income. This article provides a complete guide to your TSP options as you near retirement.

Key Takeaways:

- Traditional and Roth TSPs offer different tax benefits—choose the right one for your retirement goals.

- Evaluate your mix of G, F, C, S, I, and L Funds as you near retirement.

- Know your options for partial, full, and monthly withdrawals to maintain steady income.

- Be mindful of RMDs and how withdrawals will impact your taxable income.

TSP Basics for Pre-Retirees

Federal employees can choose between two types of TSP accounts:

- Traditional TSP: Contributions are made pre-tax, reducing taxable income now, but withdrawals in retirement are taxed as ordinary income.

- Roth TSP: Contributions are made with after-tax dollars, meaning withdrawals (including earnings) are tax-free in retirement if certain conditions are met.

As of Jan. 1, 2025, those who are 50 and older, catch-up contributions allow you to contribute an additional $7,500 beyond the standard contribution limit of $23,500. For those ages between 60 and 63, your catch-up contribution allows an extra $10,000-- due to SECURE Act 2.0. These changes were made to help you boost retirement savings in your final working years.

Understanding TSP Investment Options

The TSP offers a variety of investment options, categorized into five core funds and lifecycle (L) funds:

- G Fund: Government securities with minimal risk and guaranteed returns.

- F Fund: Bonds that provide moderate risk and returns.

- C Fund: Mirrors the S&P 500, offering exposure to large U.S. companies.

- S Fund: Tracks smaller U.S. companies, adding higher growth potential.

- I Fund: Provides international stock exposure.

Additionally, TSP participants have the option of utilizing L Funds. These are target-date funds that automatically adjust the investment mix as you approach retirement, reducing risk over time. As retirement nears, reviewing your asset allocation is essential to ensure your portfolio aligns with your risk tolerance and income needs.

TSP Withdrawal Options

When approaching retirement age, understanding how to access your TSP funds is key. Withdrawal options include:

- In-Service Withdrawals: Available while still employed under certain conditions (age-based or hardship withdrawals).

- Partial or Full Withdrawals: Take out a portion or the entire balance after leaving federal service.

- Monthly Payments or Annuities: Provides a stream of predictable income.

- Rollovers to an IRA: Maintain tax-deferred growth while expanding investment options.

Evaluating which option best suits your retirement plan is crucial for managing long-term income and tax efficiency. It is crucial to understand all your options and see which is best for your plan moving forward, because some of these decisions can be irrevocable once implemented.

Our planning team is ready to walk you through all the options, and see which withdrawal strategy makes most sense for you and your family moving forward.

Tax Considerations and Timing

How and when you withdraw from your TSP can impact your taxes. Important considerations include:

- Traditional TSP Withdrawals: Taxed as ordinary income when withdrawn.

- Roth TSP Withdrawals: Tax-free if held for 5 years and you’re over age 59½.

- Required Minimum Distributions (RMDs): Beginning at age 73, retirees must take annual RMDs, which can significantly affect their taxable income.

Strategic withdrawal planning can help minimize your tax burden and preserve more of your retirement savings.

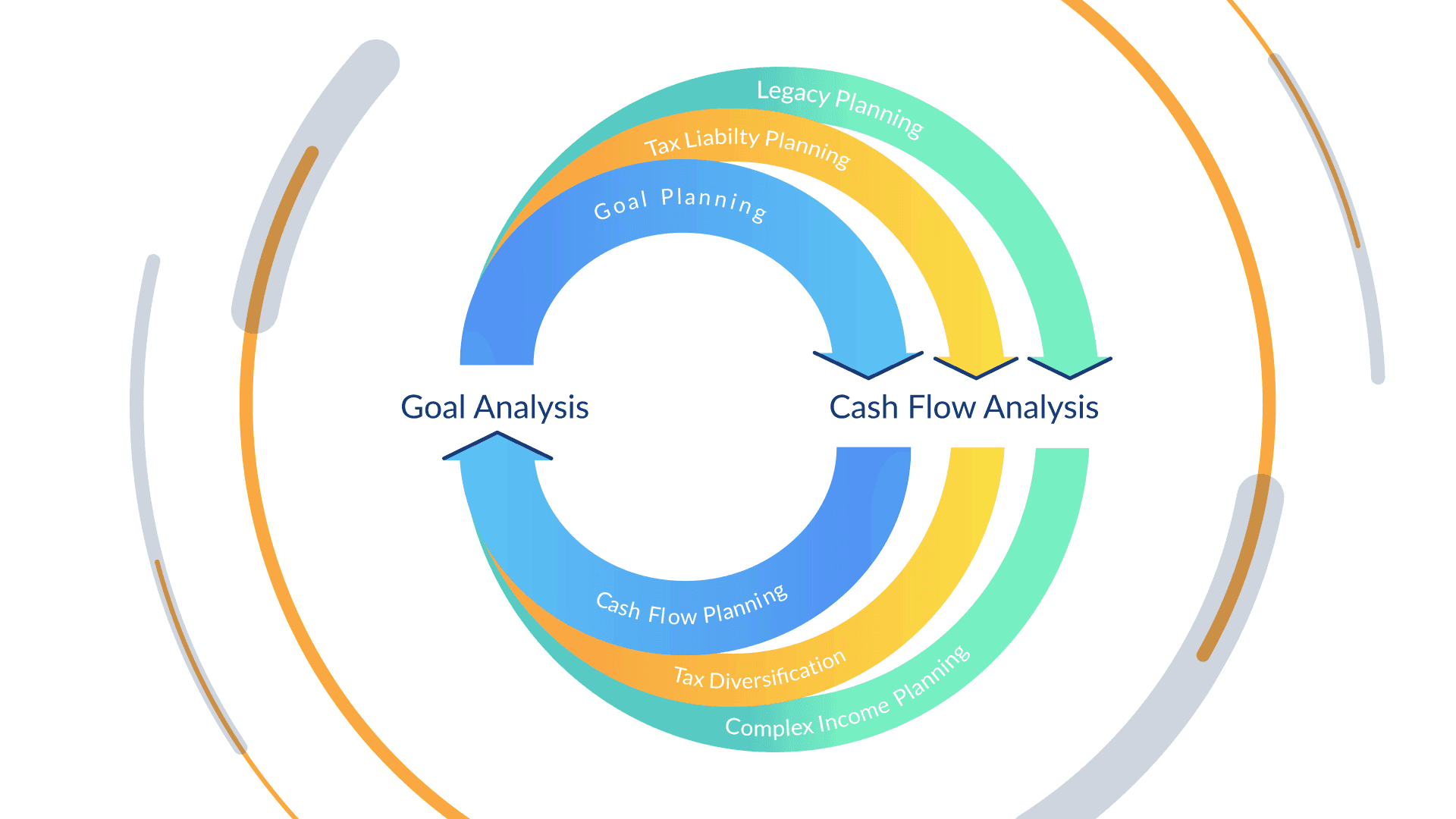

Conclusion

With ongoing directives from the current administration, it is paramount to understand your TSP options in case any drastic change occurs within your agency. Planning ahead can be a simple solution to avoid common mistakes we see every day.

To avoid pitfalls, you'll want to conduct a Portfolio DeepScan®. As you near retirement, shifting to more conservative allocations can protect against market volatility. Secondly, creating a proper withdrawal strategy is necessary to help ensure your savings will last throughout retirement & steer clear of substantial tax liabilities once RMDs kick in.

A well-balanced withdrawal strategy can help protect your nest egg and ensure a steady stream of income. Schedule a FREE Federal Retirement Readiness Review today and see where you stand.

Sources:

Thrift Savings Plan (TSP) Official Site:

https://www.tsp.gov/

TSP Withdrawal Options Overview:

https://www.tsp.gov/withdrawals/

Contribution Limits and Catch-Up Contributions:

https://www.tsp.gov/making-contributions/contribution-limits/

This article is provided by McAdam LLC dba RetireUS for informational purposes only. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this article is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax, or legal advice. Certain information contained in this report is derived from sources that McAdam believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. Opinion piece disclosure: This article is the sole opinion of this individual and is not indicative of the firm’s belief.

Related articles