Planning for Retirement: 4 Steps for a Resilient Retirement®

Planning for retirement is a multi-step, time-consuming process. You'll need to develop a plan to fund a resilient retirement, achieve financial freedom, or aim for FIRE (financial independence retire early).

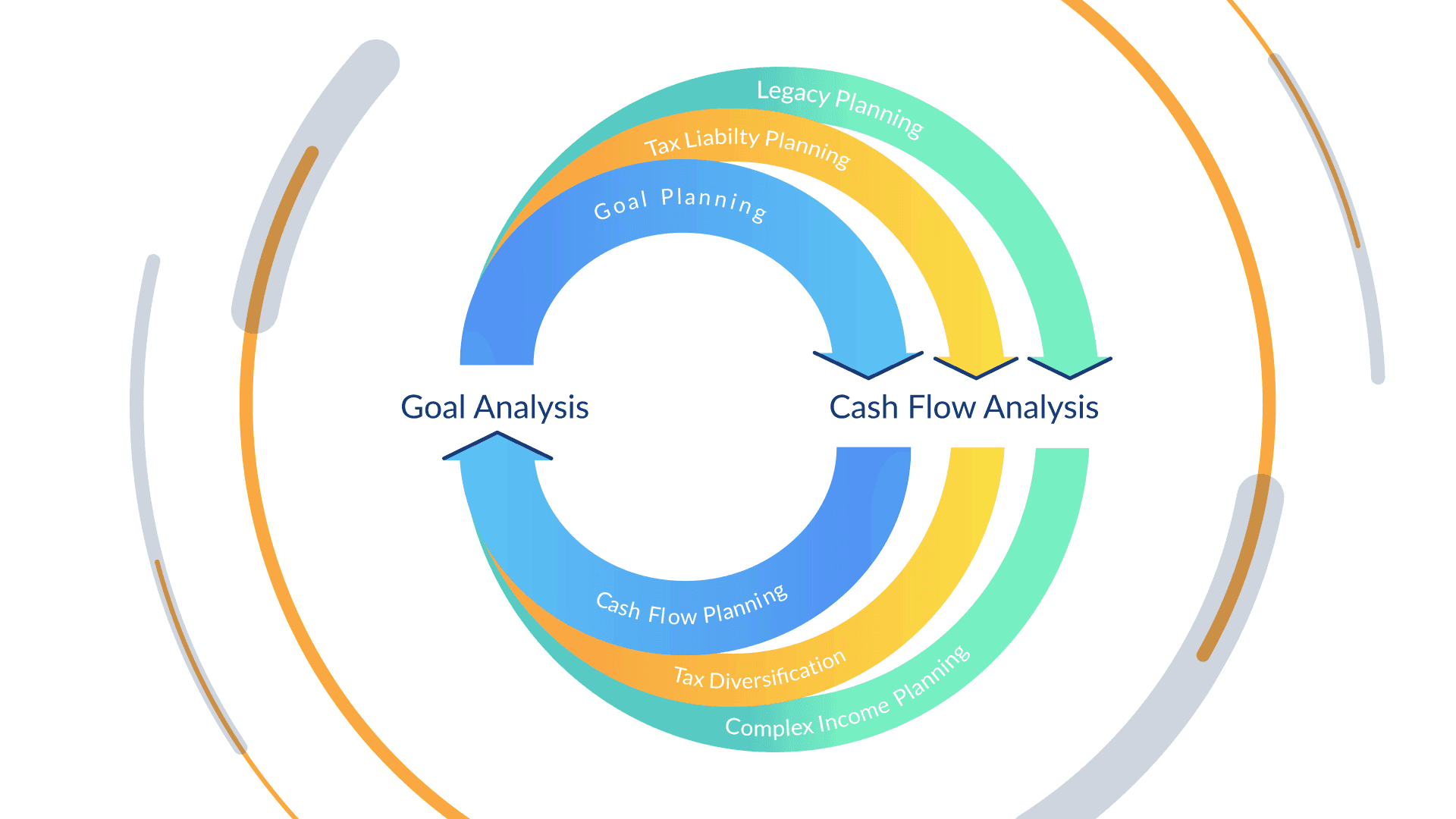

Thinking about your retirement objectives and how long you have to achieve them is the first step in retirement planning. Then, you must consider the many types of retirement vehicles that help you invest the funds needed to support your future. Once you align on what accounts to use, then income mapping has to be planned for.

- What is a 401(k) versus IRA?

- Is a Roth IRA better than a Traditional IRA?

- Is an annuity better than an IRA?

Many folks assume that because they are maxing out their 401(k) they are in good shape for retirement, but the equation is far more complex.

The final factor revolves around risk. You want to make sure your investment accounts aren’t taking on too much risk or heavily exposed to a market crash.

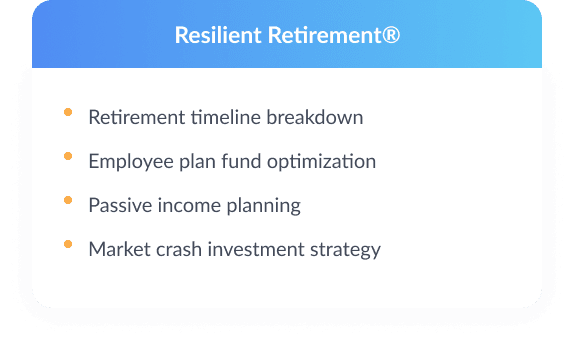

The 4 Steps in a Resilient Retirement strategy can help boost your progress towards not only retirement, but a FIRE (financial independence, retire early) lifestyle.

1. Retirement timeline: When should I retire?

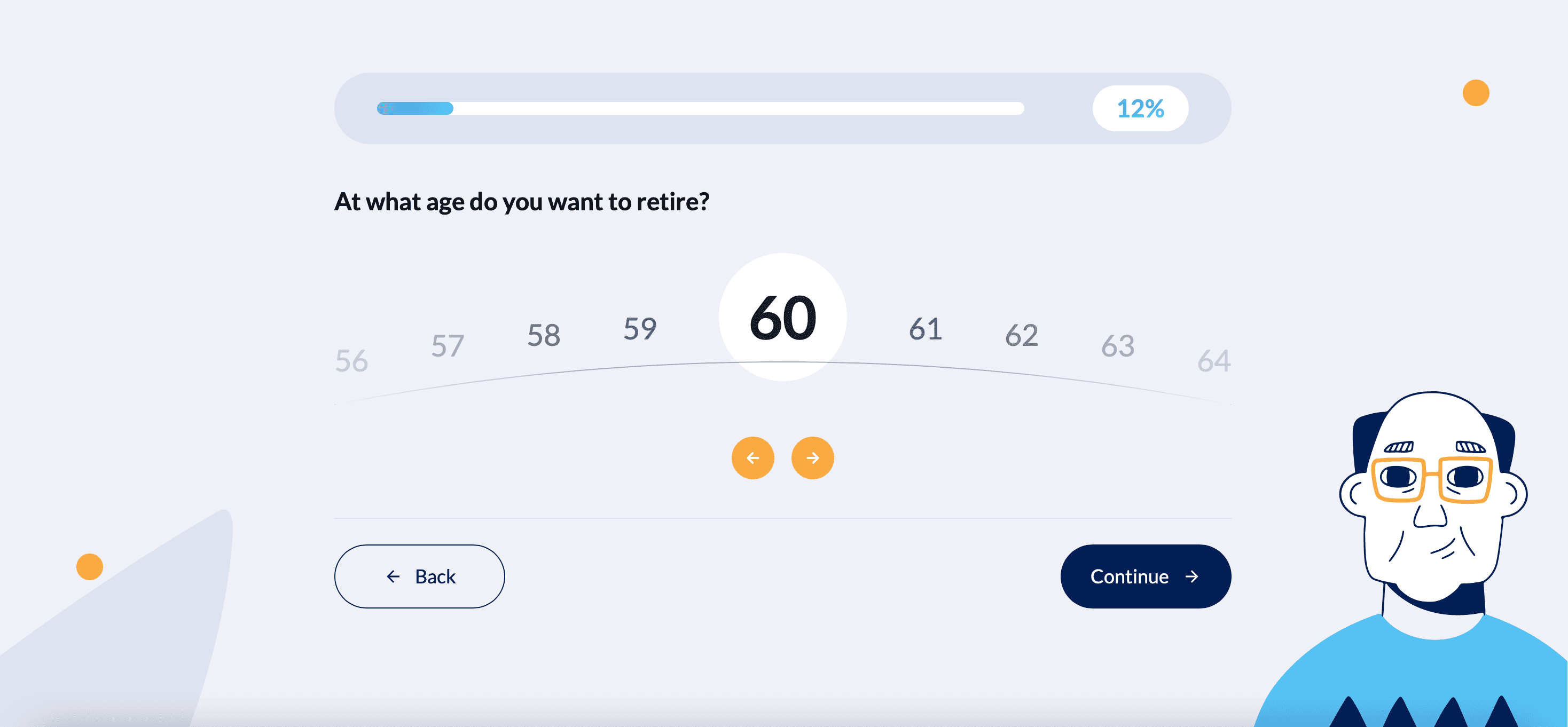

The primary foundation of a successful retirement strategy is determined by your present age and predicted retirement age. For some folks, retiring as early as 60 is something they strive for-- but others are more than okay with continuing to work until 65 or even 70!

Part of a Resilient Retirement is looking at different retirement age scenarios to see what ages make sense. Pre-65 can be difficult with high private healthcare costs, but without quantifying out what retirement will cost, how do you know if you can retire then or not?

Now for some, waiting for 65 to 67, or “Full Retirement Age”, usually revolves solely around getting the most out of your Social Security-- the longer you wait to turn on Social, the larger the monthly payouts.

Choosing an age is important when planning for retirement, so it is vital to prepare and quantify costs for different retirement ages to see what works, and what doesn’t!

Not sure when to retire? Worried about if you are on pace to retire when you want to? Use our FREE Financial Checkpoint to gauge your current progress towards retirement. Click here to start today!

2. How does a 401(k) work: Optimizing Employer plans

Understanding how your 401(k) works is very important-- and our Resilient Retirement® strategy helps optimize all of your employer plans.

First of all, we should go over how you are contributing to your 401(k). Most employers offer a match to your contribution-- according to CNBC, the average match is between 4% and 5%. If you aren’t maxing out your 401(k) ensure you are saving up to the match.

- Example: If you make a $100,000 salary and your employer matches 5%, you should contribute at least $5,000 to you 401(k), for a total contribution of $10,000.

Some plans have basic retirement age target date funds that become more and more conservative the closer it gets to the target year.

- Example: a 2025 retirement-age based fund will be much less risky than a 2050 fund. One will be allocated more into bond funds, while the other will have more equity positions, respectively.

Hopefully your plan has more options than just the standard age-based funds. If you do, it is important to know which ones can offer more growth and diversification, but also keep in mind fund costs & expense ratios.

Optimizing your 401(k) is a necessity for proper retirement planning--especially if it is your main vehicle for saving for retirement and the main account you will withdraw from.

3. What is Passive Income?

There are 2 major ways to utilize and plan around passive income-- income from investments and income from property.

Passive Income from Investing

There are plenty of ways to help generate income from investment using different products, funds, and accounts. This type of passive income can derive from dividends from stocks, ETFs, & mutual funds. It can also come from coupons of bonds & structured products. Annuities can also be set up to be used as an income instrument.

Passive Income from Properties

Generating income from properties can also be a great way to boost your income in retirement. This includes owning rental properties and using the rent payments as income (once the property is paid off). You can also purchase and resell properties and utilize the proceeds for income.

Positioning your future income in retirement beyond your Social Security and 401(k) can help maximize your nest egg and boost a FIRE lifestyle.

4. How do I Protect my Investments from a Market Crash?

If you aren’t sure how much to save for retirement, there’s a good chance your allocation may not be properly set up either. The last step in a Resilient Retirement® strategy is to make sure your investments are positioned in a way that they aren’t too exposed to a market crash.

Now, if you’re 40 years old, you can take on relatively more risky investments because you won’t be withdrawing from these retirement accounts for quite some time.

On the other hand, a 60-year-old who plans to retire in the next few years is going to be more risk averse and should be positioned in less volatile investments like bonds or annuities. If the equities were to decline over the next few years, older folks can benefit from their non-equity assets being less volatile.

As you get older, your portfolio should be more focused on income and capital preservation. This means putting more money into less risky funds & products. These investments won't provide you the same returns as stocks but will be less volatile and less susceptible in the event of a market crash.

Not sure if your investments can withstand a market crash? Use our Portfolio DeepScan® tool to get an in-depth analysis on how your accounts will match up against market downturns. Click here to learn more!

How do I get a Resilient Retirement Strategy?

Individuals are bearing more of the burden of retirement preparation than ever before, and as a result the retirement age in the USA is on the rise. The national transition from pensions to more plans like a 401(k) implies that you, not your employer, will be in charge of planning for retirement. Taking in account what age you should retire, how your 401(k) works, income strategies, & how to avoid a market crash-- there’s a lot to plan around.

It is essential to focus on building a flexible plan that can be assessed on a frequent basis to reflect changing market circumstances. Especially if you want to achieve your retirement goals or have the financial freedom to FIRE (financial independence retire early).

All of our plans include the Resilient Retirement strategy and CERTIFIED FINANCIAL PLANNER™ expertise. Click here to compare our plans to see which is best for you!

Related articles