Why You Should Rollover your 401(k) into an IRA

Picture yourself in these situations:

Your employer was just acquired, what happens to your 401(k) plan? Or, you've decided to keep climbing the career ladder and are starting a new role at your 3rd company in 7 years, what should you do with your old 401(k) accounts?

These are just 2 examples of situations where you can take advantage of a 401(k) Rollover into an IRA. A lot of people aren’t aware of how these situations can play out, so this article with break down what 401(k) rollover is, why you should rollover your 401(k), and how to do it.

What is a Rollover 401(k)?

A rollover 401(k) is a transfer of funds from your former employer's 401(k) plan into a new IRA (Individual Retirement Account) without incurring taxes or penalties.

This process preserves your hard-earned retirement savings, gives you greater control over your investments, and enables you to consolidate multiple retirement accounts for easier management. Rollovers can be done into an IRA, offering flexibility and potential for continued tax-deferred growth.

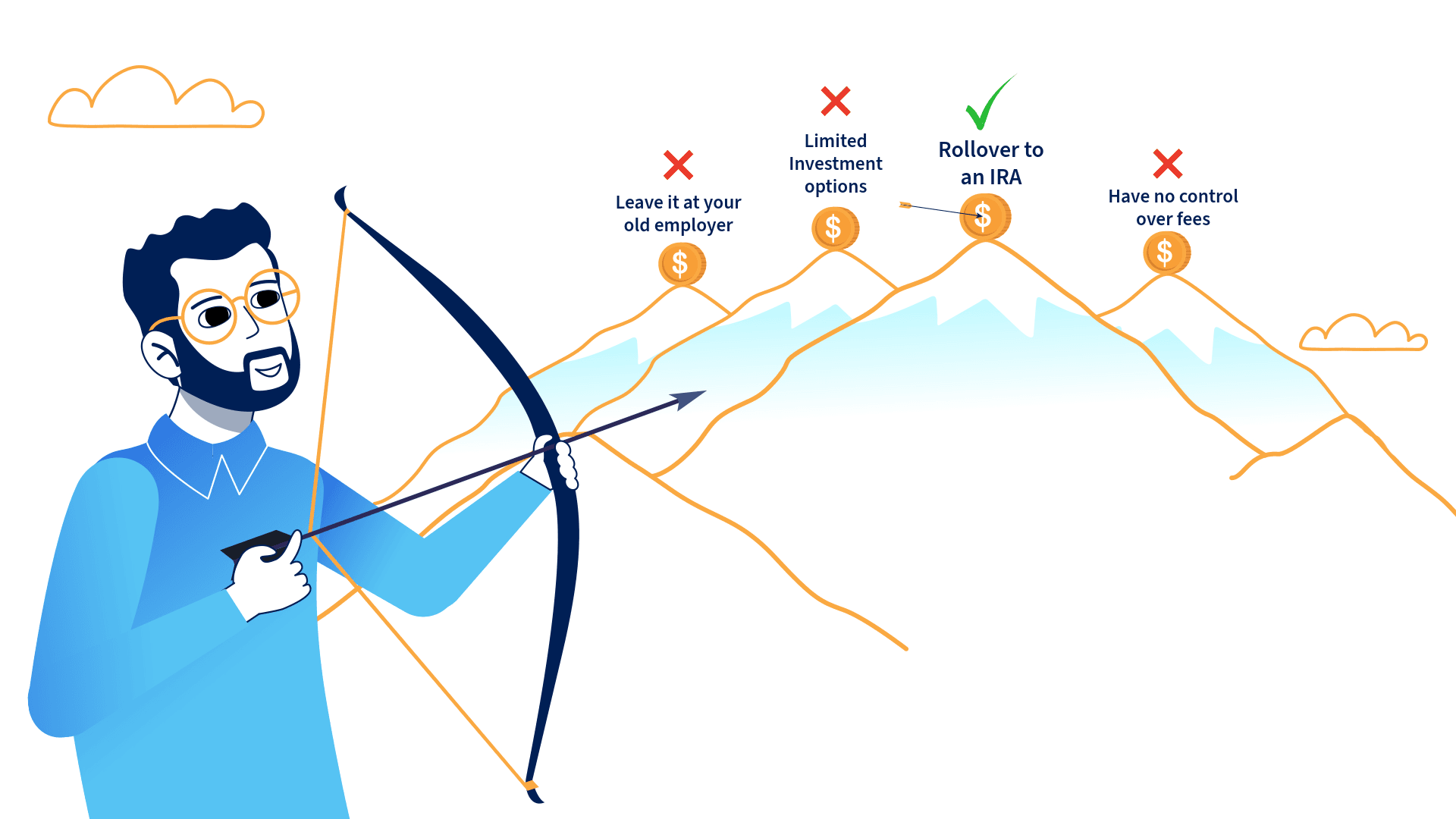

Here are three reasons why you should roll your 401(k) into an IRA:

Ownership of your 401(k)

Your 401(k), or old employer sponsored plan, is a great vehicle to save for retirement. It allows you to aggressively save for the future while taking advantage of tax-deferred growth. But the downside of an employer-sponsored plan is that you are just a participant. The plan determines how you can invest your money, whether it's limited to certain mutual funds, a specific fund company, or a particular fund share class based on your employer.

When you rollover your 401(k) into an IRA, you become the decision-making authority on how and where you can invest your savings. The IRA is an Individual Retirement Account which vastly opens the spectrum of investment options for your retirement.

Flexibility of your Rollover 401(k)

As the owner of an IRA, you:

- Have the ability to invest your retirement savings how you see fit.

- Are no longer limiting your savings to the investment stipulations of your employer sponsored plan.

- Pick and choose investments that are directly in line with your financial goals and concerns.

The Rollover 401(k) is great for both folks nearing retirement, as well as those with a longer time horizon.

The conservative investor can allocate their old 401(k) into more non-equity investments. Choosing this in preparation of market corrections offers financial protection with minimal market risk. with an employer’s plan you only get a handful of conservative fund options.

For investors who are willing to take a greater risk, you have the choice to invest in virtually any stock, ETF, mutual fund, or structured product-- much more flexibility to help boost the growth of your savings.

Cost Savings of a Rollover 401(k)

Common costs of employer-sponsored plans include administrative fees, sales charges, management fees, and other associated fees. There are several types of investment fees for 401(k) plans:

- Commissions or loads

- Transaction costs for buying and selling shares.

- Investment advisory fees & account maintenance fees

- The most common fees for managing the assets of an investment fund.

- Other fees include record keeping, furnishing statements, and customer service.

- They are billed either as a flat fee or in relation to the amount of assets invested with the funds.

How much does a 401(k) Rollover cost?

The RetireUS SimpleRollover® is free of any further costs beyond management fees-- making it very cost effective for Americans to gain expert, CFP® advice on their old 401(K) plans.

Click here to meet with an advisor and start your rollover today!

How do you Rollover a 401(K)?

On top of being free, the RetireUS SimpleRollover® is exactly that, simple! Click here to start the process by filling out this form. Once the form is complete, we will initiate the rollover process and help you gain ownership of your old 401(k), access more flexible options, and save your account from unnecessary costs with only a couple of virtual meetings.

This article is provided by McAdam LLC (“McAdam” or the “Firm”) for informational purposes only. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this article is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax, or legal advice. Certain information contained in this report is derived from sources that McAdam believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. This article is the sole opinion of this individual and is not indicative of the firm’s belief. Projected savings presented may vary depending on client longevity, and performance of assets over time.

Related articles